The Saudi quick commerce market is moving from a convenience perk to a baseline service expectation. Research cited by Maven Insights links this shift to near-universal connectivity, a highly urbanized population, a young consumer base, and a digitalized payment ecosystem. Those conditions make it easier for shoppers to place small, urgent baskets and for operators to coordinate dispatch at short notice. The same research also ties the broader environment to infrastructure investments under Vision 2030, which helps create what it describes as a digital-first setting where ultra-fast delivery can thrive.

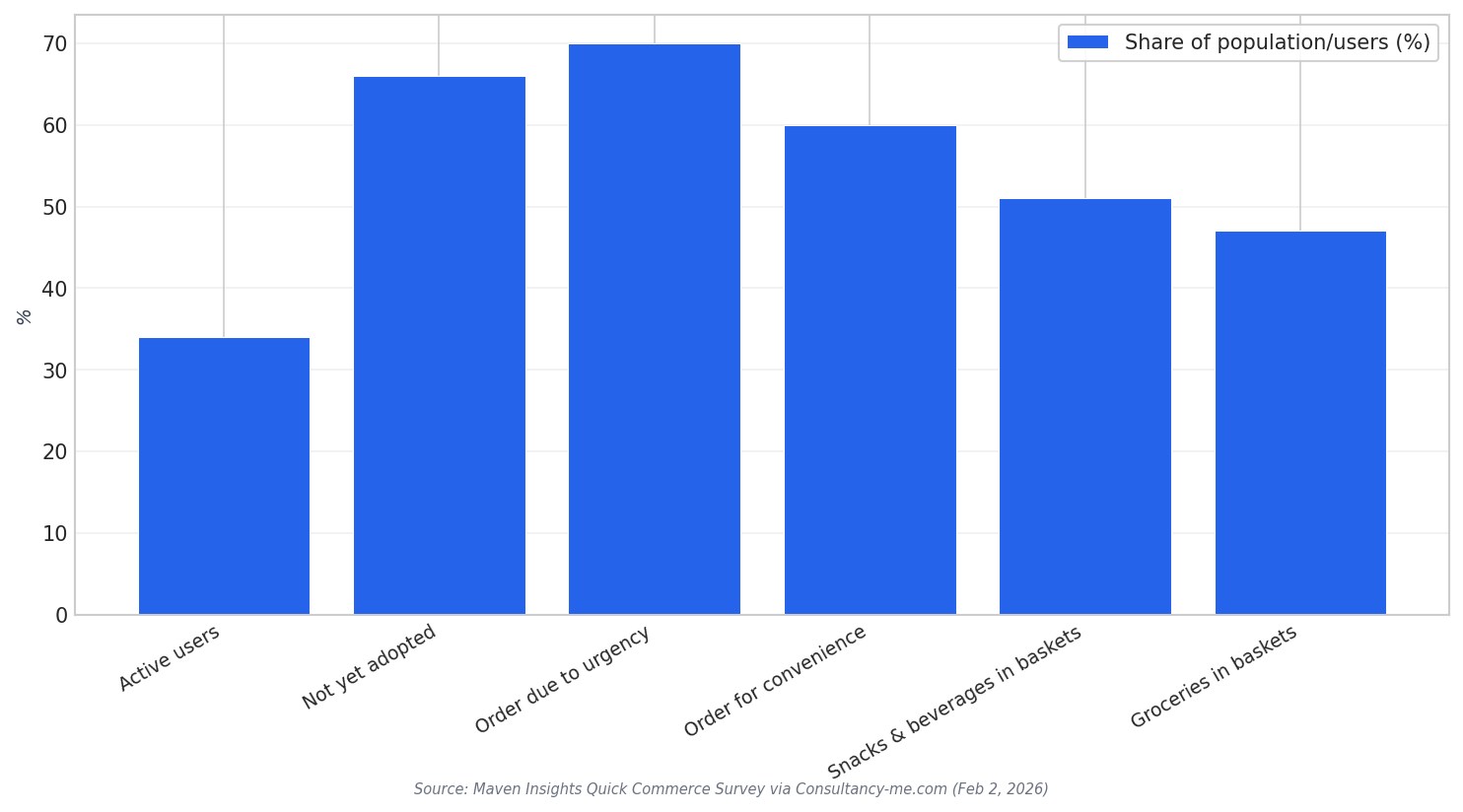

Adoption is already meaningful, but the runway is still large. Maven Insights reports that 34% of the population are active users of quick commerce services, while 66% have not adopted the habit. Among users, the leading driver is urgency: about 70% order because they need an item urgently. Convenience is also a major motivator at around 60%. These motivations matter for grocery retail because they point to last-minute and top-up missions rather than large weekly shops, pushing grocers and platforms to win the “right now” moment.

Why the “15-Minute” Race Changes Grocery Retail

The race toward ultra-fast delivery is not unique to Saudi Arabia, but it clarifies the operational bar grocery retailers are being judged against. Business Insider reporting on ultrafast delivery highlights the physical and financial demands of making a 15-minute promise, with a supply chain consultant arguing there is “probably not as much of a market for anything under 30 minutes.” The same reporting notes that retailers face constraints rooted in “the laws of physics and finance.” For Saudi grocery retail, this frames speed as a strategic choice that must be balanced with cost, reliability, and service coverage.

In Saudi Arabia, Maven Insights suggests the next chapter is operational excellence, where efficiency turns into trust. That is directly tied to grocery outcomes: every on-time delivery and accurately filled order becomes a proof point for consumers who value their time. Basket data also shows grocery is already central to quick commerce usage, with groceries appearing in 47% of delivery baskets, alongside snacks and beverages at 51%. At the same time, the research flags a growth opportunity beyond core grocery, as users want small home appliances, fitness gear, and clothing available for rapid delivery.

Cost perception is a key barrier to converting the 66% who do not yet use quick commerce in Saudi Arabia, according to Maven Insights. That matters for grocers and platforms deciding how aggressively to compete on speed, assortment, and fees. Operational efficiency can also be pursued inside traditional retail. For example, Arab News reports BinDawood Holding agreed to acquire a 51% stake in Vaza Food Co. for SR217.9 million ($58.06 million), with BinDawood stating the deal may generate operational efficiencies through improved procurement and logistics and consolidation of certain support functions. While not a quick commerce metric, it illustrates how grocery retailers are seeking efficiency and supply-chain strength as consumer expectations rise.

What is driving adoption in the Saudi quick commerce market?

How many people are using quick commerce services in Saudi Arabia?

Why do users place quick commerce orders in Saudi Arabia?

What items show up most often in Saudi quick commerce baskets?

Is 15-minute delivery always realistic for retailers?