The EU’s Carbon Border Adjustment Mechanism (CBAM) is moving from a reporting exercise to a cost-and-competitiveness test. The transitional phase runs from 1 October 2023 to 31 December 2025, where importers report emissions but do not pay charges. The definitive regime starts on 1 January 2026, when financial obligations begin and roll out over a nine-year period through the purchase and surrender of CBAM certificates linked to embedded greenhouse gas emissions. This is the core Saudi Arabia EU CBAM carbon border tax impact: exporters can no longer treat emissions data as optional paperwork, because verification and documentation become part of commercial access to Europe.

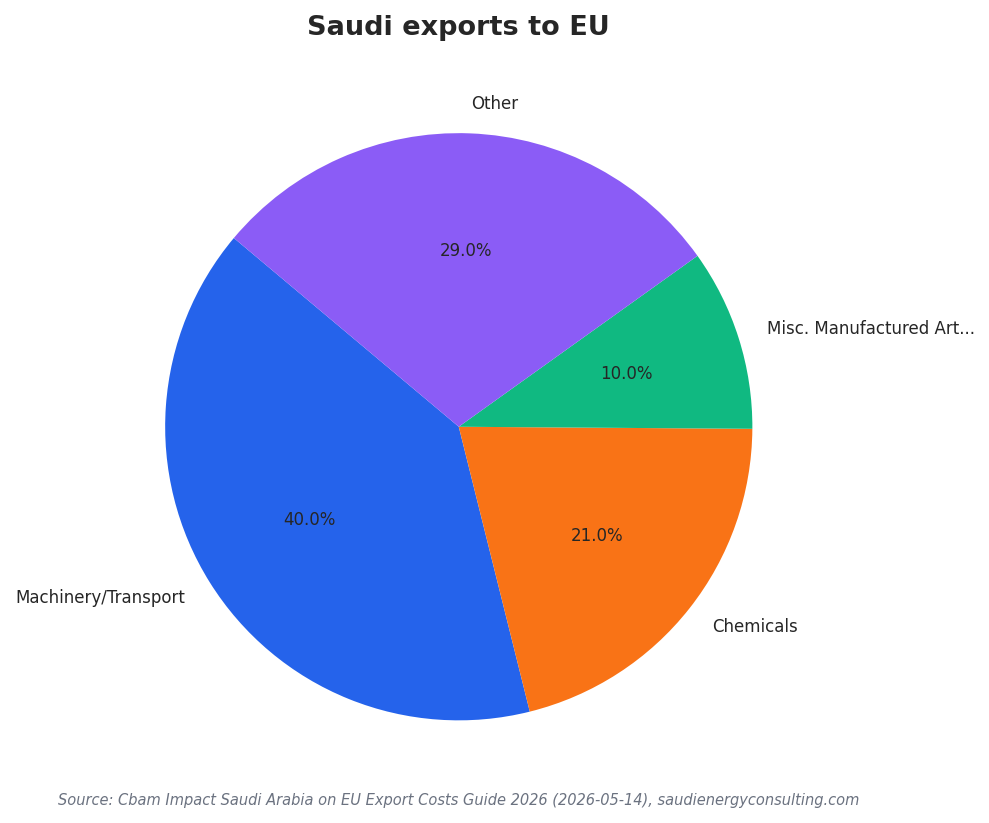

The stakes are large because the trade relationship is large. In 2024, total bilateral goods trade between Saudi Arabia and the EU reached about €69.9 billion. Imports from Saudi Arabia to the EU were €33.07 billion, while exports from the EU to Saudi Arabia were €36.84 billion. Saudi exports to the EU grew 7.5% year-on-year from 2023 to 2024, while imports from the EU dropped 9.5%. Chemicals were a major Saudi export category at €7.86 billion (21%). Machinery/Transport was €14.7 billion (40%), and Miscellaneous Manufactured Articles were €3.57 billion (10%). Even small delays or reporting errors can become meaningful when trade volumes are this high.

What Changes on 1 January 2026: Costs, Certificates, and Thresholds

From 2026 onwards, EU importers must be authorised CBAM declarants if they import more than a single mass-based threshold of 50 tonnes of CBAM goods into the EU. They will buy CBAM certificates from national authorities, with certificate prices calculated based on the auction price of EU ETS allowances expressed in €/tonne of CO2 emitted. In 2026, the price is set as a quarterly average, and from 2027 onwards as a weekly average. Importers declare embedded emissions and surrender the corresponding number of certificates annually. If they can prove a carbon price was already paid during production in the country of origin, the corresponding amount can be deducted.

For Saudi exporters, the practical pressure is not only the payment signal, but the proof burden. During the transitional phase, EU importers must submit quarterly CBAM reports covering quantities imported, embedded direct and indirect emissions, and any carbon pricing applied in the country of origin. For carbon costs, a regional assessment cited for the Arab region estimates 70 to 95 Euros per ton of CO2 emitted under the EU ETS, and warns that without domestic decarbonisation reforms and mitigation efforts, competitiveness in the European market will dwindle. Saudi petrochemical-linked value chains, metals, and cement face heightened scrutiny, and reported hurdles include complex Scope 1 and Scope 2 measurement and the need for verification under EU-recognised standards such as ISO 14064-3 and ISO 17029.

Exposure also varies by product mix and CBAM coverage. The European Commission lists initial CBAM goods as cement, iron and steel, aluminium, fertilisers, electricity, and hydrogen. In Gulf Cooperation Council context, one analysis finds that in 2023 the UAE exported US$2.7 billion worth of CBAM-covered goods, Bahrain US$1.3 billion, Saudi Arabia US$565 million, and Oman US$400 million, concluding Saudi Arabia and Oman face more moderate exposure while Kuwait and Qatar are largely unaffected. Under current rules discussed in that analysis for aluminium, only direct and precursor emissions are covered, and it states GCC aluminium production CO2 intensity is similar to the EU and lower than China and India, which can make CBAM-related price increases comparable to EU producers and lower than some competitors. Still, separate Saudi-focused analysis frames a readiness risk as “Institutional Translation Debt,” estimating Saudi Arabia’s Translation Debt at €116.5M tied to gaps in MRV systems, third-party verification capability, and domestic carbon-pricing infrastructure needed to defend carbon performance in regulated markets.

When does CBAM shift from reporting to payments for EU imports?

How big is Saudi Arabia–EU goods trade, and why does CBAM matter for it?

What is the mass-based threshold for requiring an authorised CBAM declarant?

What does the Saudi Arabia EU CBAM carbon border tax impact look like for costs and competitiveness?

How exposed is Saudi Arabia compared with other GCC exporters under CBAM-covered goods?