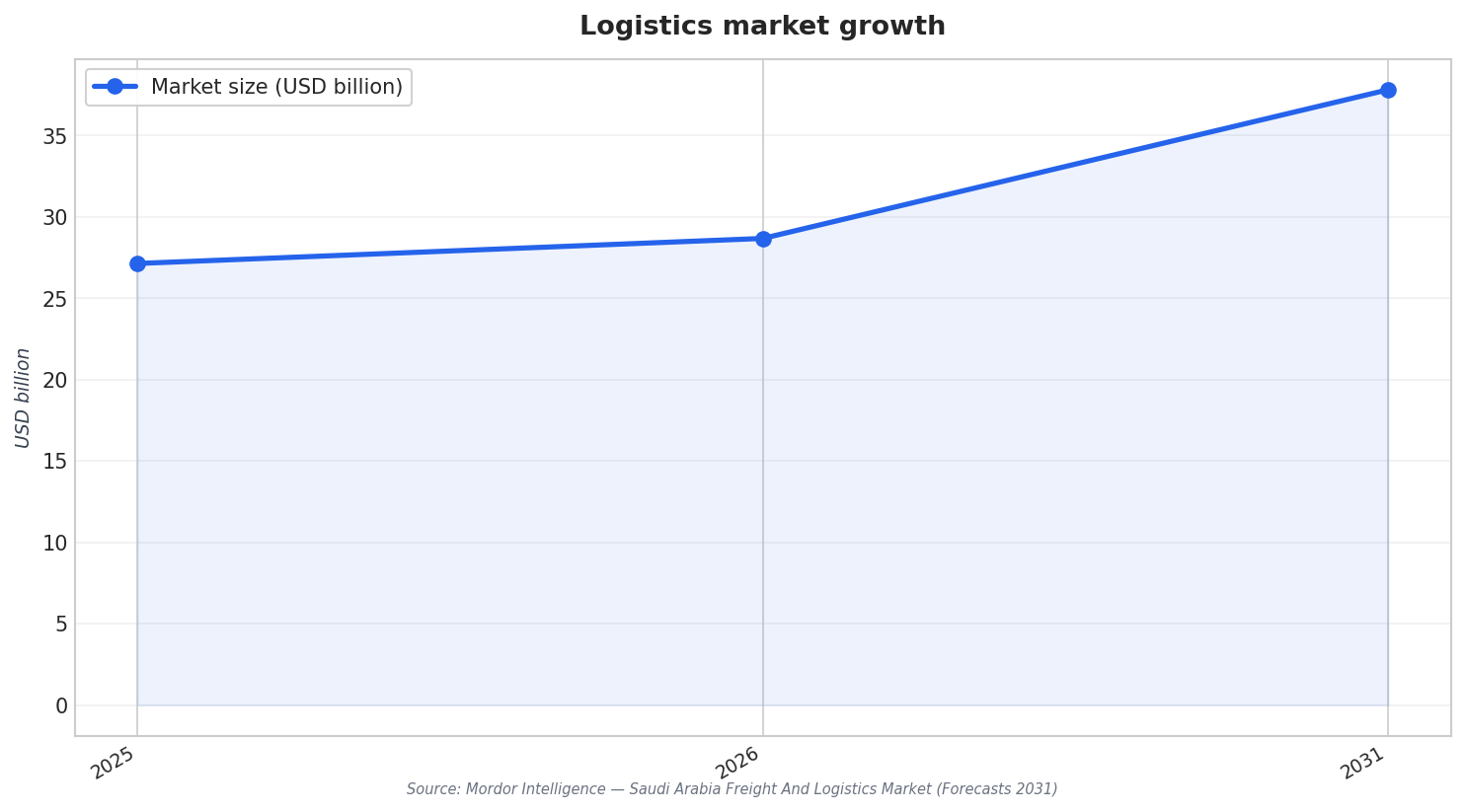

Saudi Arabia’s logistics sector is in a speed contest. Global e-commerce inflows are pushing networks to behave less like traditional freight corridors and more like always-on parcel systems. Market signals show why. Mordor Intelligence values the Saudi Arabia freight and logistics market at USD 27.14 billion in 2025, with an estimate of USD 28.68 billion in 2026 and a forecast of USD 37.82 billion by 2031 (2026–2031 CAGR: 5.69%). In 2025, freight transport captured 58.92% of market share, while Courier, Express, and Parcel (CEP) services are forecast to advance at a 6.45% CAGR between 2026 and 2031. These shifts matter for Saudi Arabia cross-border e-commerce fulfillment because international parcels compress timelines, increase scan-and-track expectations, and raise the penalty for customs or sorting delays.

Capacity building is the centerpiece of the response. Mordor Intelligence links Vision 2030’s infrastructure drive to USD 133.3 billion of approved airport, rail, and port outlays, and highlights bonded-zone e-commerce hubs as a lever that accelerates cross-border fulfillment efficiency. Policy also influences who can move freight and how quickly services modernize. Mordor Intelligence notes a gradual removal of cabotage-like restrictions for foreign carriers that permits international operators to serve domestic line-haul lanes previously reserved for Saudi-flag fleets. The same report says DSV’s 29-facility network already handles 6% of Saudi import volumes, illustrating how scale and digital visibility can compete for time-sensitive flows. Ken Research separately notes KSA’s plan to establish 59 logistics zones by 2030 as part of the National Transformation plan.

Where Cross-Border Demand Hits Hardest: CEP, Air, and Fulfillment Nodes

The biggest operational pressure shows up where parcels meet cities. In CEP, Mordor Intelligence reports that domestic deliveries represented 65.05% of segment revenue in 2025, but international CEP traffic is projected to grow at a 6.69% CAGR between 2026 and 2031. Mode choice is also evolving. Road freight held a 41.55% revenue share in 2025, yet air freight is projected to expand at a 6.78% CAGR over 2026–2031, a mix that fits cross-border parcel needs when speed is worth the premium. Warehousing also reflects a split between today’s footprint and tomorrow’s requirements: non-temperature-controlled warehouses dominated with a 77.25% share in 2025, while temperature-controlled capacity is forecast to climb at a 6.48% CAGR (2026–2031), aligning with Mordor’s note that cold-chain investments are rising alongside pharmaceutical import growth and tourist-driven fresh-produce demand.

Contract logistics is adapting with facilities and process design built for customs and returns. Mordor Intelligence describes multimodal nodes inside planned logistics centers with bonded storage, automated cross-docks, and customs one-stop shops, which intensify demand for end-to-end contract logistics agreements. The same source says Saudi customs agency ZATCA scrapped all export service fees in October 2024, lowering the cost of cross-border fulfillment for local merchants. In market sizing, Mordor Intelligence values the Saudi Arabia contract logistics market at USD 1.23 billion in 2025, with an estimate of USD 1.27 billion in 2026 and a forecast of USD 1.51 billion by 2031 (2026–2031 CAGR: 3.52%). It also notes Riyadh and its surrounding Central Province generate the highest contract logistics spend, supported by a population above 7 million and automated fulfillment centers that anchor national distribution.

Competition is forcing operators to differentiate, not just discount. Market Report Analytics describes pricing pressure from numerous global and local entrants, with e-commerce platforms negotiating aggressively and last-mile delivery often facing the highest margin pressure due to high fixed costs. At the same time, it notes that warehousing and fulfillment services that leverage advanced automation and integrated solutions can command better margins by offering inventory management, packaging, and labeling. Ken Research frames the e-commerce logistics stack as broader than delivery alone, including transportation, warehousing and inventory management, value-added services such as labeling, packaging, and returns management, fulfillment centers, last-mile delivery, and cold chain logistics. This is the strategic end state of the race: faster customs-to-customer flows, better visibility, and node-based networks that can flex with international parcel surges.

What is driving Saudi Arabia’s push to improve cross-border e-commerce fulfillment?

How fast is international CEP traffic expected to grow in Saudi Arabia?

Which logistics capabilities are being built into planned logistics centers?

What policy change affected export costs for local merchants shipping cross-border?

Why are margins under pressure for e-commerce logistics providers in Saudi Arabia?