Saudi Ramadan consumer spending is best understood as a rhythm, not a rush. In the GCC, retailers are rethinking engagement during the month, moving away from large-scale spectacles and toward targeted activations and operational improvements that match how customers live. Landmark Group, which operates multiple mid-tier fashion brands under Centrepoint, describes Ramadan unfolding in phases. Early demand centers on preparation, with home and wardrobe purchases leading the cycle. The final weeks then bring a surge in gifting and celebratory dressing. This phased pattern helps explain why Ramadan remains a cornerstone event in the retail calendar rather than a short-lived seasonal blip.

In practice, that rhythm can be quantified inside retailer customer bases. Landmark board member Nisha Jagtiani said roughly 70 percent of the retailer’s top customers nearly double their shopping frequency during Ramadan. That detail matters for planning, because frequency shifts can strain fulfillment, staffing, and store operations if teams only prepare for higher average baskets. The strategic takeaway is that Ramadan is “the beginning of the conversation,” not the end, as Jagtiani put it, and brands that only “show up once a year” risk looking inauthentic to customers who expect deeper cultural understanding.

Timing also reshapes buying behavior and merchandising decisions. Ramadan 2026 is expected to begin around February 18 or 19, depending on moon sighting, with Eid al-Fitr falling in the third week of March. That early timing creates what Majid Al Futtaim Lifestyle CEO Fahed Ghanim called a “genuine compression of the retail calendar,” because it comes just weeks after the holidays and nearly collides with Valentine’s Day (February 14) and Lunar New Year (February 17). For the first time in a century, Lunar New Year and Ramadan begin almost exactly the same time, adding execution pressure for global brands running parallel playbooks.

Retail Strategy: Plan for Phases, Locality, and Selective Spend

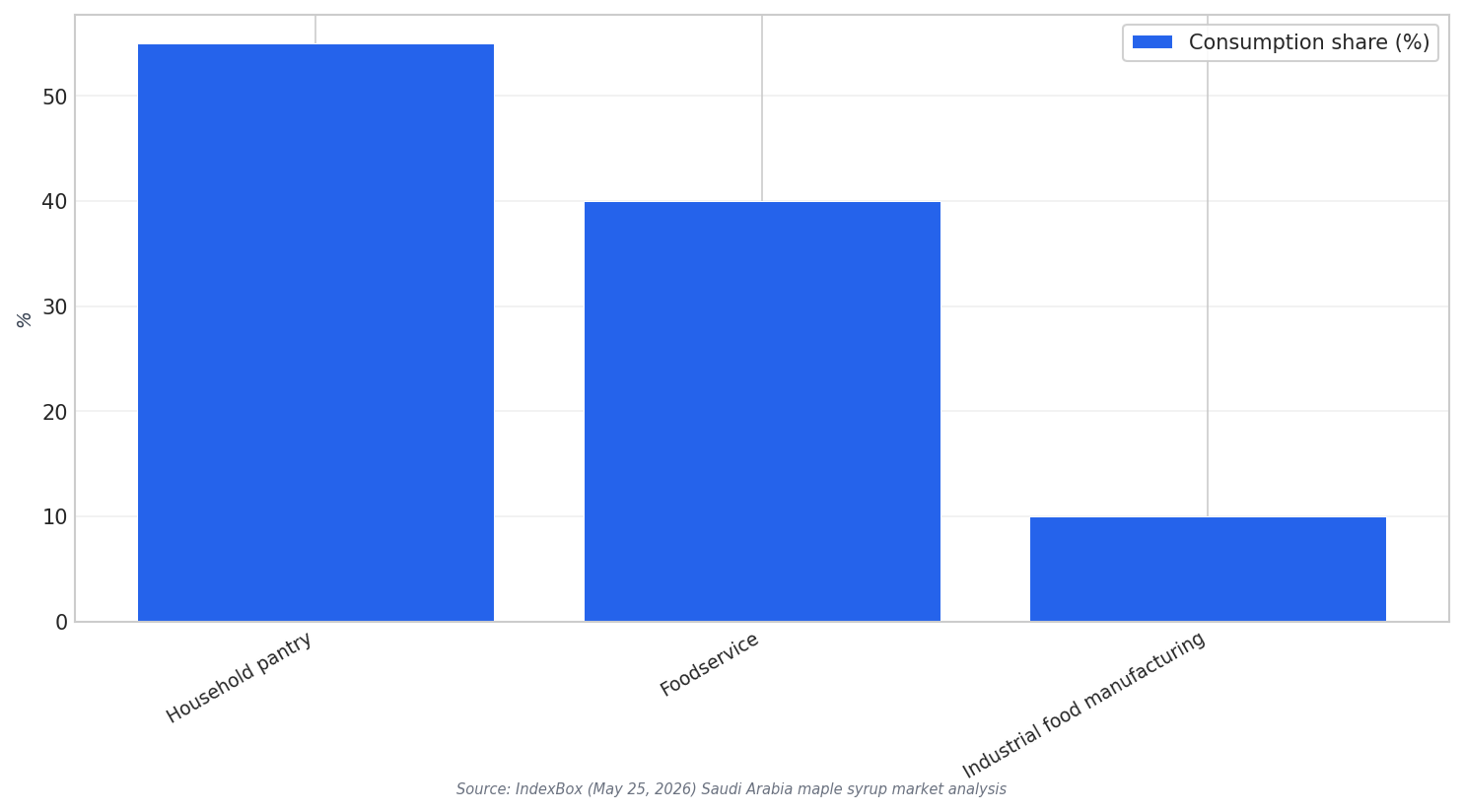

Retailers can also learn from adjacent seasonal demand signals in food and gifting. In Saudi Arabia’s maple syrup market analysis, the household pantry is the largest consumption channel at about 50–55% of volume. Foodservice follows at 35–40%, and industrial food manufacturing accounts for 5–10%. The same analysis notes foodservice demand is seasonal, with consumption spiking during Ramadan for suhoor and iftar pancakes. It also argues seasonal and gifting applications are under-developed, citing Ramadan gift baskets and corporate hampers as margin opportunities, and suggesting a domestic bottling approach could reduce final retail mark-up by 15–20%.

In fashion and broader retail, Saudi-specific expectations are rising. Saudi Fashion Commission CEO Burak Çakmak said “Thirty-five million local population is a very different engagement,” and warned against treating the market with an expat mindset. He added that a Ramadan capsule “no longer suffices,” because consumers want to shop for every occasion, not just Ramadan. On the mall side, Cenomi’s 2026 Ramadan and Eid trading outperformed 2025 by double digits in both footfall and retail sales. Yet Majid Al Futtaim’s Khalifa Bin Braik described a “recalibration in spending priorities,” with consumers becoming more deliberate and selective, which should shape assortment depth, promotions, and clienteling.

What does “Saudi Ramadan consumer spending” look like in phases?

How much does shopping frequency change during Ramadan for top customers?

Why is Ramadan 2026 operationally challenging for retailers?

What signals suggest Saudi shoppers are becoming more selective?

What is one under-developed Ramadan retail opportunity mentioned in the sources?