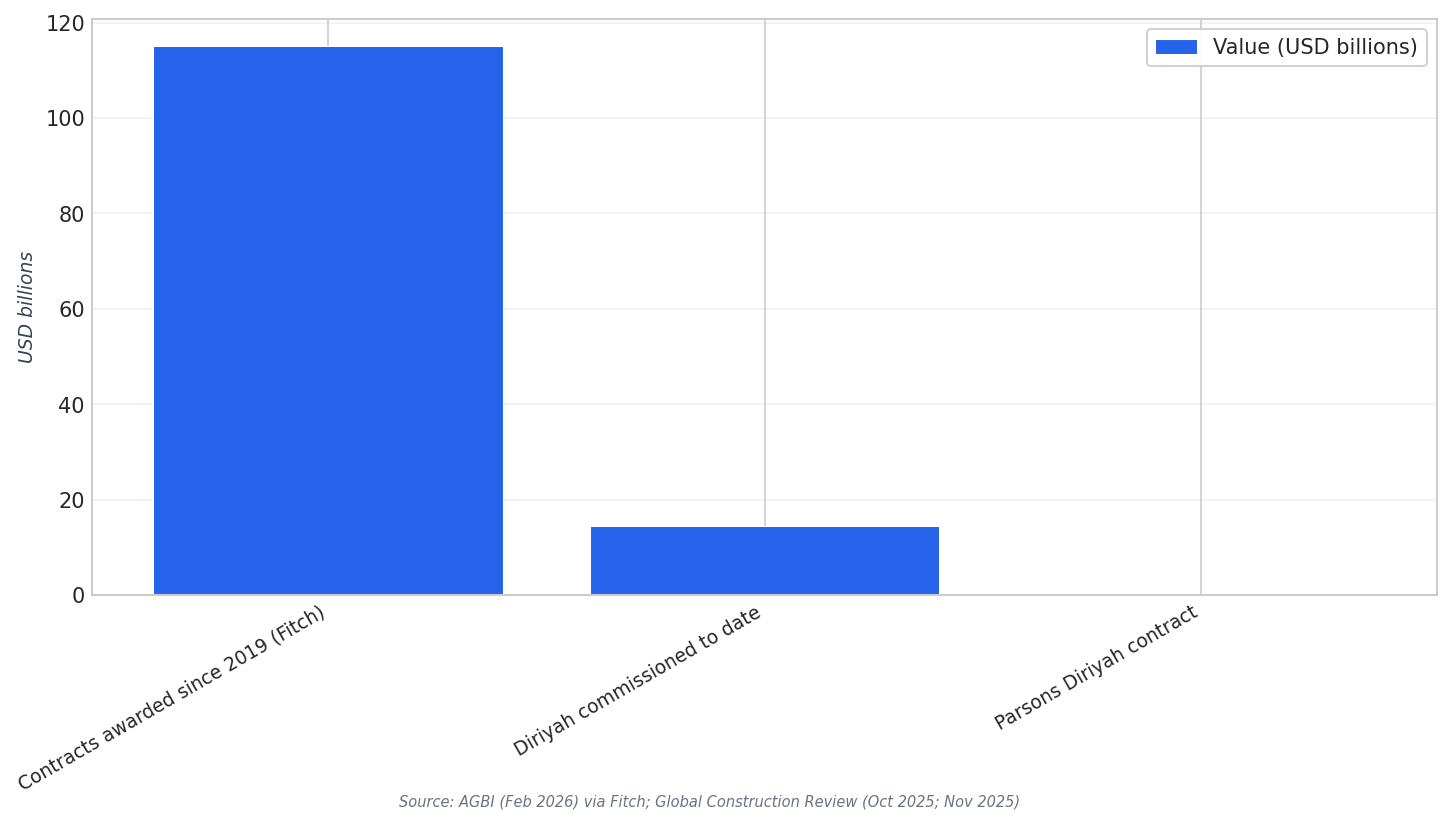

Saudi giga projects are entering a recalibration phase, not a simple stop-start cycle. Multiple reports describe a pivot in priorities, a review of scopes and timelines, and a push to bring in more private capital. Fitch Ratings estimated that only $115bn worth of giga-project contracts have been awarded since 2019. Fitch also said roughly half of total funding, including debt and capital, has been coming from the Public Investment Fund (PIF), positioning it as a financier of last resort for parts of Vision 2030. In October, investment minister Khalid Al Falih said the giga-projects “have been taking a lot of resources from the government” and urged local and foreign investors to step in.

The near-term signal is prioritisation. A new investment protocol puts Expo 2030 and the 2034 World Cup at the top of the priority list, according to AGBI. One person with direct knowledge of the tenders pipeline said: “No contract of significance is going to be awarded this year unless it’s got the words Expo or World Cup.” The same source added this includes transportation, mobility and energy infrastructure, and entertainment tied to these events. For contractors, that points to tighter bid funnels and clearer packaging around event-led infrastructure, rather than a broad, simultaneous release of unrelated packages.

Financing and liquidity dynamics are now part of delivery risk. The Architects’ Journal reported that contractors and consultants are waiting longer for payments while many projects are financially recalibrated due to rising construction costs, timeline pressures, AI, and shifting priorities such as hosting the 2034 World Cup. A senior individual quoted there said PIF-controlled projects rely on funds from the sale of hydrocarbons and that, with oil prices under pressure, there is a squeeze on liquidity. Fitch expects banks’ giga-project financing to grow, but warned this could pressure banks’ capital because they must set aside more to mitigate higher risk-weightings for the developments.

What Changes for Contractors: Pipeline Discipline, Not Empty Work

Pipeline discipline does not mean the work disappears. Global Construction Review cited a consultant view that annual contract awards in Saudi Arabia rose to $196bn, up 20% from 2024. It also described Riyadh as leading on giga projects with developments such as Diriyah Gate, King Salman Park and the 220km Sports Boulevard. Diriyah Gate was described as a $63bn cultural project, with commissioned projects to date at $14.5bn and a further $45.6bn in the pipeline. Separately, Global Construction Review reported Diriyah is undergoing a $63.2bn transformation, and that Parsons won a $56m five-year design and construction supervision contract for the next phase, covering parks, open spaces, and more than 55km of streetscapes.

For investors, the message is that governance, sequencing, and returns are being pulled forward. AGBI reported PIF governor Yasir Al Rumayyan said in October the fund was in the final stages of approving a revised investment strategy for 2026-2030, with a fuller version expected in the spring after investor feedback. A person familiar with PIF finances said the roughly $1tn sovereign wealth fund is likely to cut capital spending by up to 15%. Mining.com also described a broader push for greater discipline in capital allocation and said PIF will step up efforts to boost returns, following months of spending decisions, including reviews of projects like Neom and a pivot toward areas more likely to attract foreign investment.

This recalibration is also changing how advisory and intermediated delivery is funded. Consultancy-me reported Saudi Arabia ordered government entities to cut back, and in some cases freeze, payments to management consultants, while also halting awarding new contracts to many consulting firms. The same report said several projects had already begun undergoing reassessment before the recent regional conflict escalated, citing rising costs, financing requirements, and lower-than-expected international investor appetite. It quoted Finance Minister Mohammed al-Jadaan as stating the kingdom had “no ego” about revisiting projects and adjusting plans. For contractors and investors, the practical takeaway is to expect more direct, partnership-led models and stronger scrutiny of value, payment terms, and bankability.

What is driving the recalibration of Saudi giga projects?

Which projects are being prioritised in the new tender pipeline?

How does the funding mix affect contractors and banks?

What should investors watch in the next strategy cycle?

What does this mean for contractors bidding on Saudi giga projects?