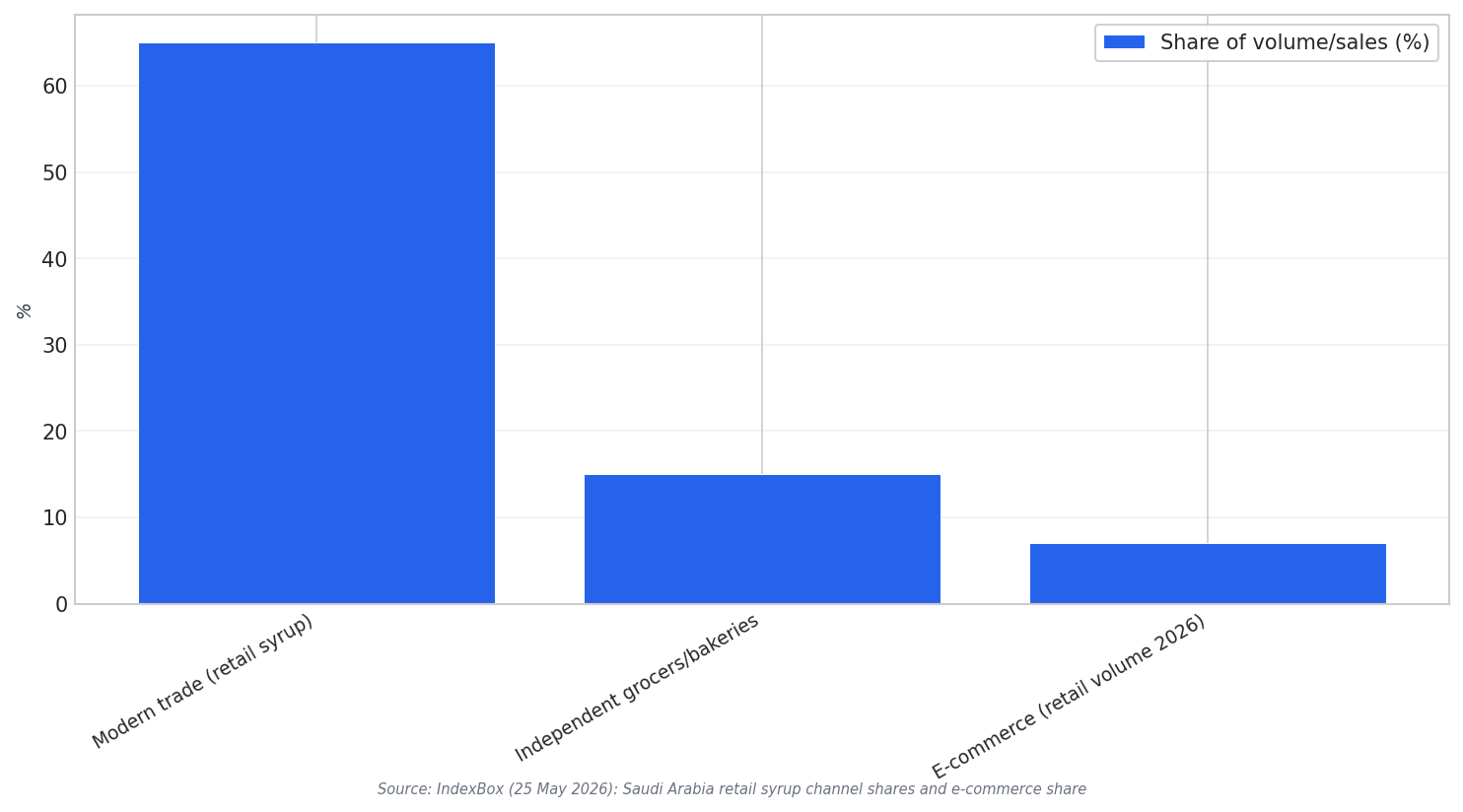

In 2026, a usable Saudi Arabia distribution strategy starts with mapping where demand actually sits and then deciding who should carry the operational load. A clear example of a multi-channel setup appears in retail syrup: modern trade and supermarkets account for an estimated 60–65% of retail syrup sales, while independent grocery stores and bakeries handle 10–15% of volume. E-commerce is described as the fastest-growing channel, but still only 5–7% of retail volume in 2026. This mix matters because it influences whether you need an agent for access, a distributor for execution, or a direct model for control.

The same source shows how channel requirements differ by customer type and pack format. Foodservice distributors serve hotels, restaurant chains, and catering companies, and supply bulk formats such as 3–5-litre bag-in-box, sometimes alongside branded tabletop bottles. That channel is growing 8–10% annually, linked to the expansion of Western-style brunch spots and hotel buffet breakfast offerings. For many categories, this is a hint that a specialized distributor can create speed and reach in foodservice, while modern trade demands strong merchandising execution across hypermarkets and supermarkets.

Based on these 2026 channel shares, leaders can pressure-test three go-to-market options. An agent-led model can fit when your priority is introductions and negotiations with modern trade accounts that represent 60–65% of retail syrup sales. A distributor-led model can fit when you need warehousing, delivery, and multi-customer coverage, including foodservice buyers where growth is 8–10% annually. A direct model can fit when you want to build your own e-commerce and key-account capabilities, especially as e-commerce is 5–7% of retail volume in 2026 and projected to reach 12–15% by 2035.

How to Choose the Right Model for 2026 Execution

Model selection is also an operational readiness question, not only a commercial one. AIM notes that identifying and qualifying regional distributors, logistics providers, and local representatives is time-consuming and requires due diligence, contracting, and onboarding. AIM also recommends starting the process early, well before any commercial launch, so supply chain readiness does not become the critical path bottleneck. To keep execution structured, AIM recommends a launch team across four workstreams: supply planning, production readiness, logistics management, and distribution partnership.

Direct models become more realistic when you can build local capability and support cross-border flows. A Reuters/Zawya item on Unilever’s new OMO Liquid line in Saudi Arabia describes a digitally enabled facility that will act as a Middle East hub, with more than half of production confirmed for export to regional markets and the rest serving local demand. At the macro level, PwC’s Economy Watch summary notes that non-oil sectors account for around 56% of Saudi Arabia’s SAR 4.7 trillion economy. Together, these points support a 2026 strategy that evaluates local operations, export ambition, and the control-versus-speed trade-off when choosing between agents, distributors, and direct routes.

What is a practical Saudi Arabia distribution strategy for 2026?

When does a distributor model make the most sense in Saudi Arabia?

How fast is e-commerce growing in Saudi retail channels?

What operational steps should companies plan before launch?

What evidence supports building more direct capability in Saudi Arabia?