Saudi Arabia has qualified 24 local and international companies and consortiums to compete for exploration licenses across three multi-mineral belts. The Ministry of Industry and Mineral Resources framed the move as part of broader efforts to develop the mining sector, increase exploration spending, and attract high-quality investment. The licenses target gold, silver, copper, nickel, and zinc, and the ministry’s communications repeatedly link exploration activity to an estimated mineral resource value of SR9.4 trillion ($2.5 trillion). The signal for investors is not only the size of the opportunity narrative, but also the visible depth of the applicant pool now willing to pass technical and financial evaluation.

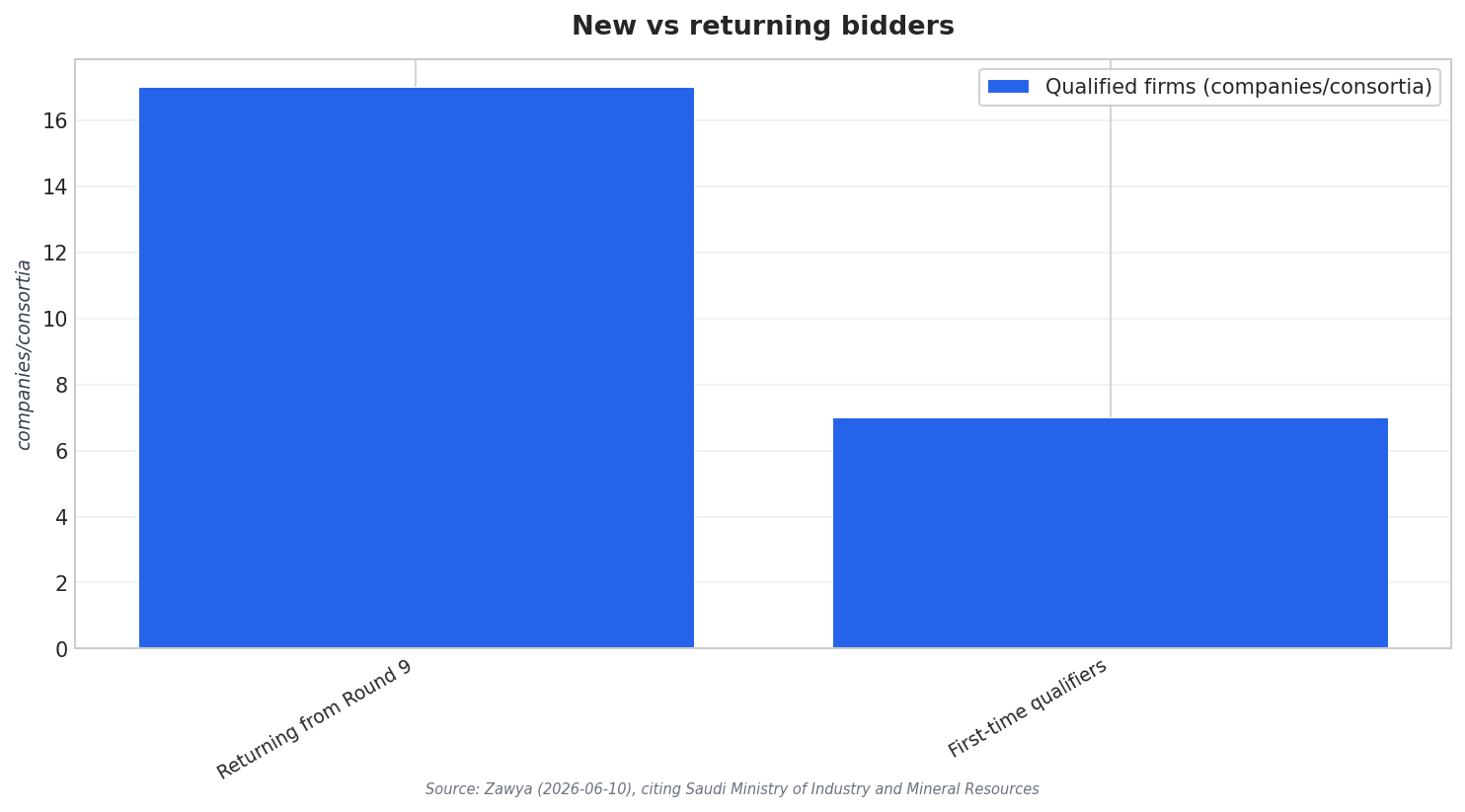

Round 10’s competitive field is also telling because it is not entirely new. Officials said the 24 qualified bidders include 17 participants from the previous round, plus seven companies qualifying for the first time, a change described as reflecting the growing attractiveness of Saudi Arabia’s mining investment environment. In practical terms, that blend suggests continuity in how serious bidders are approaching the Kingdom while also widening the funnel of potential new entrants. The round covers three belts spanning 13,000 sq km, and the next phase will see qualified bidders select available exploration sites through the Taadeen platform.

What the 24 Qualified Bidders Reveal About Demand, Commodities, and Process

The roster and belt descriptions show why the competition is multi-commodity rather than single-metal. The Al-Nuqrah Belt is described as known for significant gold deposits and copper- and zinc-rich volcanic massive sulfide mineralisation. Alongside Al-Nuqrah, coverage referenced the Sukhaybarat-Al-Safra belt as part of the round’s multi-commodity character, reinforcing why bidders can align strategies to precious metals and base metals at the same time. Zawya listed examples of previously pre-qualified participants under Round 9, including India’s Vedanta, Australia’s Midana Exploration, Jacaranda Minerals, and DesertEx, US-based Sierra Nevada Gold, and Saudi entities such as Royal Road Arabia.

To interpret the Round 10 opportunity, it also helps to view it against the immediately prior benchmark. The ministry said its ninth exploration licensing round had 24 companies and consortia winning licenses and described it as the largest in the Kingdom’s history to date. The ministry also said Round 9 offered over 24,000 km2 spanning the Ad-Duwaihi/Nabitah gold belt in the Riyadh region, as well as the Nuqrah and Sukhaybirah/As-Safra gold belts in the Madinah and Qassim regions, with strategic minerals including gold, copper, silver, zinc, and nickel. A separate market summary of Round 9 stated 172 mining sites were awarded and that coverage also said the round covers 24,000 square kilometers.

For companies tracking Saudi Arabia mining exploration licenses 2026, the most actionable takeaway is that the Kingdom is building repeatable participation mechanics. Discovery Alert described a staged competitive framework that prioritises technical credibility and financial capacity, supported by a digital platform approach that can let companies assess options without committing to an expensive in-country presence during pre-qualification. Zawya also stated that Round 10’s next phase runs through Taadeen site selection, reinforcing the role of the platform in execution. At the same time, commentary noted that some remote areas, including parts of Hail and northern Qassim, may require material capital investment beyond direct exploration costs, which bidders must factor into program design.

How many firms qualified for Saudi Arabia’s Round 10 exploration licenses?

How large is Round 10 in geographic coverage?

Which minerals are targeted in the latest Saudi exploration licensing round?

What do the Round 10 qualifiers suggest about Saudi Arabia’s mining investment pipeline?

What should companies know about Saudi Arabia mining exploration licenses 2026 when planning participation?